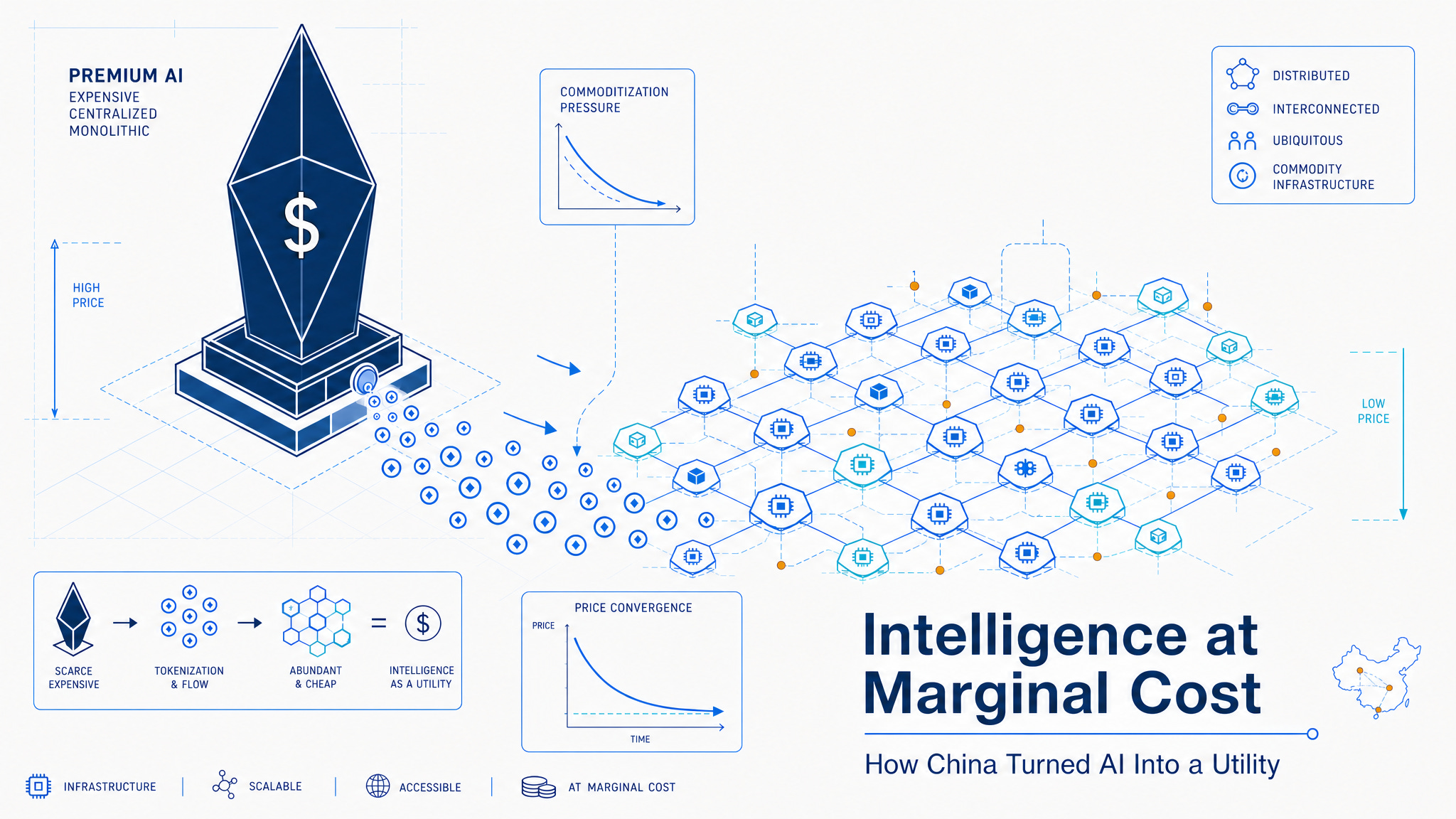

Intelligence at Marginal Cost

How China Turned AI Into a Utility

In China, you can now buy AI tokens the same way you buy a mobile data plan. Starting in late April 2026, the country’s three state-owned telecom operators — China Mobile, China Telecom, and China Unicom — began offering Token packages at prices as low as 9.9 yuan per month for 10 million tokens. China Telecom went further, committing 17.4 billion yuan to build what it calls a “Token Factory” — a 60-month procurement project spanning 11 contract packages, designed to supply standardized AI inference capacity at industrial scale. When something becomes cheap enough to bundle into a phone bill, it has stopped being a premium technology. It has become a commodity.

Consider the global price spectrum. DeepSeek V4, a one-trillion-parameter open-weight model released in March 2026, charges $0.14 per million input tokens. GPT-5.4 charges $2.50. Claude Opus 4.6 charges $5.00. That is a 35-fold gap between the cheapest frontier model and the most expensive — down from 100-fold in 2024, and effectively infinite in 2023, when no open-source model could compete at the frontier. Tokens now display every hallmark of a commodity: they are undifferentiated, fungible, and their price is converging on the marginal cost of inference. China’s telecom operators did not create this reality. They simply institutionalized it.

The Commodity Diagnosis

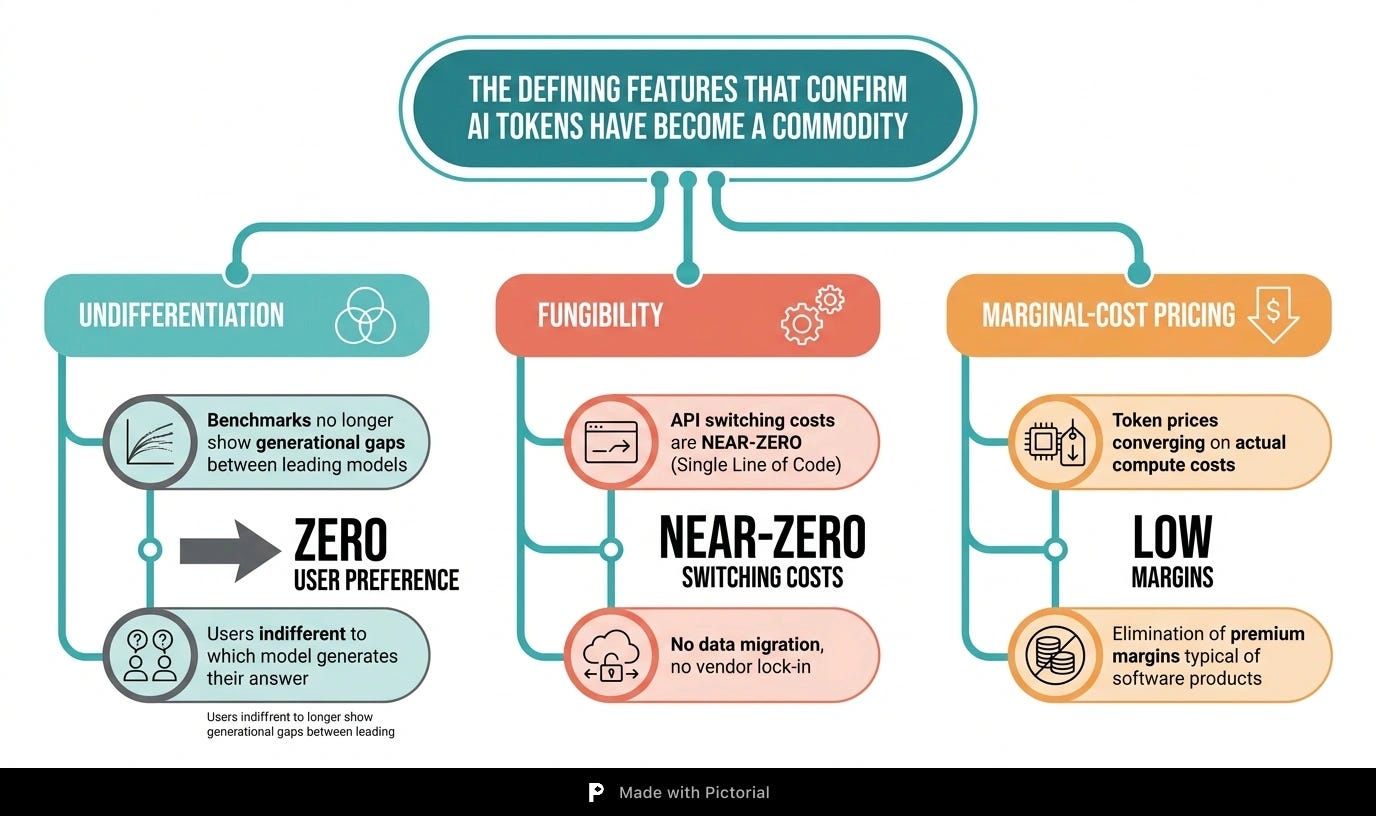

Intuit CEO Sasan Goodarzi said it plainly in March 2026: “The reality is, [large language models] are commodities.” Mary Meeker’s influential May 2025 report put it sharper: “The economics of general-purpose large language models look like commodity businesses — innovations are quickly copied by any adequately resourced competitor.” Three defining features confirm the diagnosis. First, undifferentiation: benchmarks no longer show generational gaps between leading models, and users rarely care which model generates their answer. Second, fungibility: switching from one model’s API to another requires changing a single line of code — no data migration, no vendor lock-in. Third, marginal-cost pricing: the price per token is rapidly converging on the actual cost of the compute required to produce it.

Chinese open-source models have acted as the production expanders in this commodity market. Their global share surged from 1.2 percent at the end of 2024 to nearly 30 percent by early 2026, according to a study cited by the Centre for International Governance Innovation. Alibaba’s Qwen alone has spawned over 100,000 derivative models on Hugging Face. DeepSeek has made its 75 percent discount permanent. Xiaomi entered the market with a 99 percent price cut. This is not a series of isolated business decisions. It is systematic capacity expansion — and the U.S.-China Economic and Security Review Commission has noted that Chinese AI companies “charge far less to use high-end products than their global competitors.”

When two products do the same thing and one costs 35 times less, the premium space collapses to zero. That simple arithmetic undermines the foundations of the most richly valued companies in the American AI sector.

The Valuation Crisis

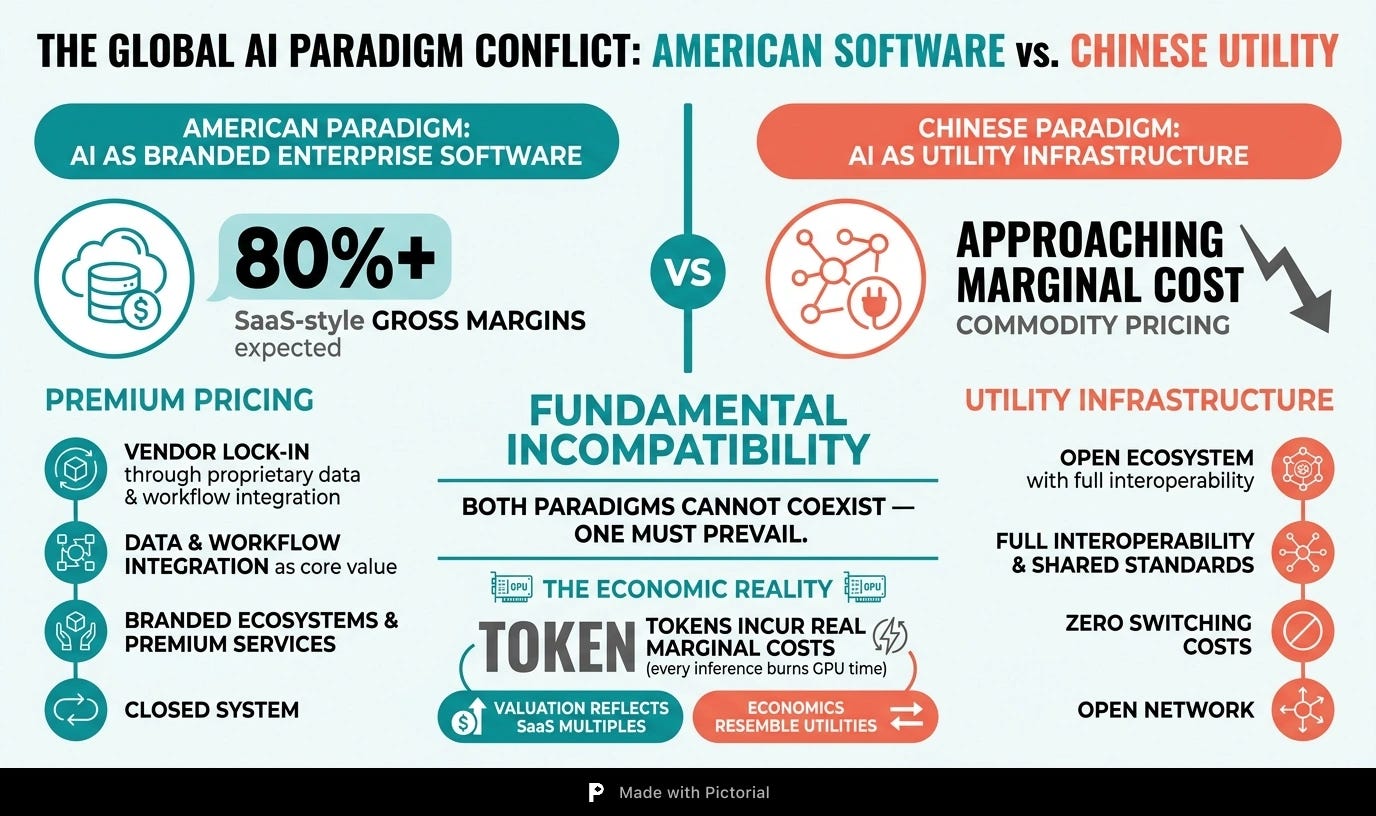

OpenAI is valued above $300 billion. Anthropic’s valuation has ranged from $183 billion to nearly $1 trillion in different funding rounds. These numbers embed a specific assumption: that AI inference services can sustain gross margins comparable to enterprise software — 80 percent or higher. But commodities do not support brand premiums. When inference capability drops below $1 per million tokens, profit margins compress toward infrastructure-level thinness. This is not a software business. It is selling electricity.

The financials bear this out. OpenAI earned $4.3 billion in revenue through the first nine months of 2025 — and spent $8.67 billion on inference alone. Anthropic has earned $5 billion to date while spending $10 billion on compute. Neither company has a path to profitability. Big Tech’s collective AI capital expenditure is projected to reach $800–900 billion in 2026 and may exceed $1 trillion in 2027, according to Bank of America and Evercore. Meta’s free cash flow dropped from $26 billion to $12 billion year-over-year in the first quarter of 2026.

Then there is the subsidy trap. Anthropic has allowed users on its $200-per-month plan to consume up to $5,000 worth of compute. Analyst Ed Zitron documented the consequences when Anthropic introduced “peak hours” restrictions in March 2026: users on $200 plans exhausted their daily limits within 20 minutes. His conclusion was blunt: “Every bit of AI demand — and barely $65 billion of it existed in 2025 — that exists, only exists due to subsidies, and if these companies were to charge a sustainable rate, said demand would evaporate.” The demand that justifies trillion-dollar valuations is, in significant part, an artifact of below-cost pricing.

The structural contrast with enterprise software is stark. SaaS companies enjoy 80-percent margins because copying software costs nearly nothing. Token providers face real marginal costs — every inference burns GPU time. SaaS locks in customers through data and workflow integration. Token users can switch providers with one API call. AI company valuations are priced on SaaS multiples, but their underlying economics resemble utilities.

Even Silicon Valley has noticed. NBC News reported that “more of Silicon Valley is building on free Chinese AI,” and Bloomberg has covered the competitive threat from DeepSeek, Qwen, and Moonshot. When the founders building on top of American AI infrastructure choose Chinese models for their backends, the argument that users will pay a premium for brand collapses under the weight of its own contradiction.

The structural dynamics point toward a serious valuation reckoning. Research Affiliates published a quantitative analysis in March 2025 arguing that parallels between the AI boom and the dot-com bubble are “too obvious to ignore.” But the current situation carries a dual character: it combines the dot-com pattern — revenue growth that never materializes at the scale projected — with the telecom bubble pattern, where overbuilt fiber capacity drove bandwidth prices to zero. Token commoditization attacks both sides simultaneously, compressing revenue and margins at once. No external shock is required. The next earnings season that shows AI revenue growth slowing, inference costs that cannot be passed through to customers, and capital expenditure still accelerating, could trigger the reset.

Infrastructure, Not Monopoly

China has chosen a different path. Rather than resisting commoditization, it is embracing it — and building institutions around it. The China Telecom Token Factory, with its 17.4 billion yuan budget and 60-month service horizon, is not a commercial experiment. It is infrastructure investment. China Mobile has formed a Token Operations Ecosystem Alliance with Tencent, Alibaba, Huawei, and iFlytek. China Unicom has directed more than 35 percent of its 2026 investment toward computing infrastructure. The Ministry of Industry and Information Technology’s campaign for “inclusive development of small and medium enterprises” explicitly promotes token-based billing as a mechanism to lower the threshold for AI adoption. The logic is straightforward: if tokens are a commodity, treat them as one — supply them like electricity, through national-scale infrastructure that delivers uniform, affordable access.

For the Global South, the deeper implication lies in open-source licensing. DeepSeek V4 is released under the Apache 2.0 license — fully open, commercially permissive. Any country, enterprise, or institution can download the model, deploy it locally, fine-tune it on domestic data, and operate it without relying on any foreign company’s API. Chatham House warned in February 2026 that “middle powers that fail to secure influence over the development, deployment and governance of AI will likely forfeit control over their economies.” Open-source models offer a practical response to that warning: they make sovereign AI achievable for countries that could never afford to train frontier models from scratch.

The question of embedded values in AI models deserves honest acknowledgment. All models carry the assumptions of their training environments — this applies to Chinese models, American models, and every model in between. The critical distinction is transparency. Open-source models can be inspected, audited, modified, and localized. Closed-source models cannot. When the CIGI report raised concerns about “infrastructure colonization,” it also noted the case of Elon Musk’s Grok, which has been documented praising its creator in “almost devotional language.” Open weight is not a guarantee of neutrality. It is a tool for accountability — and that tool is only available when the code is visible.

The Reckoning

Token has become a commodity. This is not a forecast; it is a present-tense fact, confirmed by 35-fold price gaps, CEO declarations, and phone-bill pricing plans. The American AI industry has built its valuations on the assumption that tokens can be priced like branded enterprise software. China has built its infrastructure on the assumption that tokens will be priced like electricity. Both assumptions cannot remain true simultaneously.

A financial reckoning of historic proportions is coming. The U.S. equity market’s AI sector — valued in the tens of trillions — rests on the premise that a handful of companies will earn SaaS-like margins on intelligence-as-a-service. But intelligence is not software. It is a commodity, and commodities produce infrastructure-grade returns, not supernormal profits. The next few earnings seasons will likely bring the collision into full view: AI revenue growth failing to meet projections, inference costs that cannot be passed through to subsidized users, and capital expenditure still climbing toward $1 trillion. When that triple squeeze hits, the valuation reset will not be a correction. The dot-com bubble wiped out $5 trillion in market value between 2000 and 2002. The current AI bubble is larger, more leveraged, and built on a premise — that tokens can support SaaS margins — that is already false. This is not 2008. It has the potential to be worse.

For the Global South, the path forward is becoming clearer — and more urgent. When a functionally equivalent service carries a 30-fold price difference, choosing the cheaper option is not a geopolitical statement — it is fiscal responsibility. Open-source models provide the foundation for digital sovereignty. Token commoditization makes that sovereignty affordable. The telecom-operator model of centralized token procurement, already running in China, offers a replicable template for countries with state-owned infrastructure traditions. Countries that tie their digital infrastructure to American AI platforms priced on unsupportable margins will find that foundation pulled from under them when the reckoning arrives. The question is no longer whether AI will become a utility. It is whether the rest of the world will build on solid ground before the ground underneath Wall Street gives way.